- CIT Solutions

-

A Superior Collective Investment Trust Onboarding Experience.

-

- Perspectives

- About

- Reach out

A Superior Collective Investment Trust Onboarding Experience.

A Superior Collective Investment Trust Onboarding Experience.

By Jason Levy – Sr. Counsel at Great Gray

Collective investment trusts (CITs) are now the most prevalent investment vehicle in defined contribution plans according to the Callan Institute’s 2024 Defined Contribution Trends Survey. Yet, many retirement plan decisionmakers and advisors still remain unfamiliar with CITs. Part 1 of this blog post was geared to this audience. It explained why CITs are gaining traction in retirement plans and highlighted the common types of investment vehicles available for retirement plan lineups to help better understand the choices.

For Part 2 of this blog post, I’ll dive into what makes CITs stand out as a modern retirement plan investment vehicle.

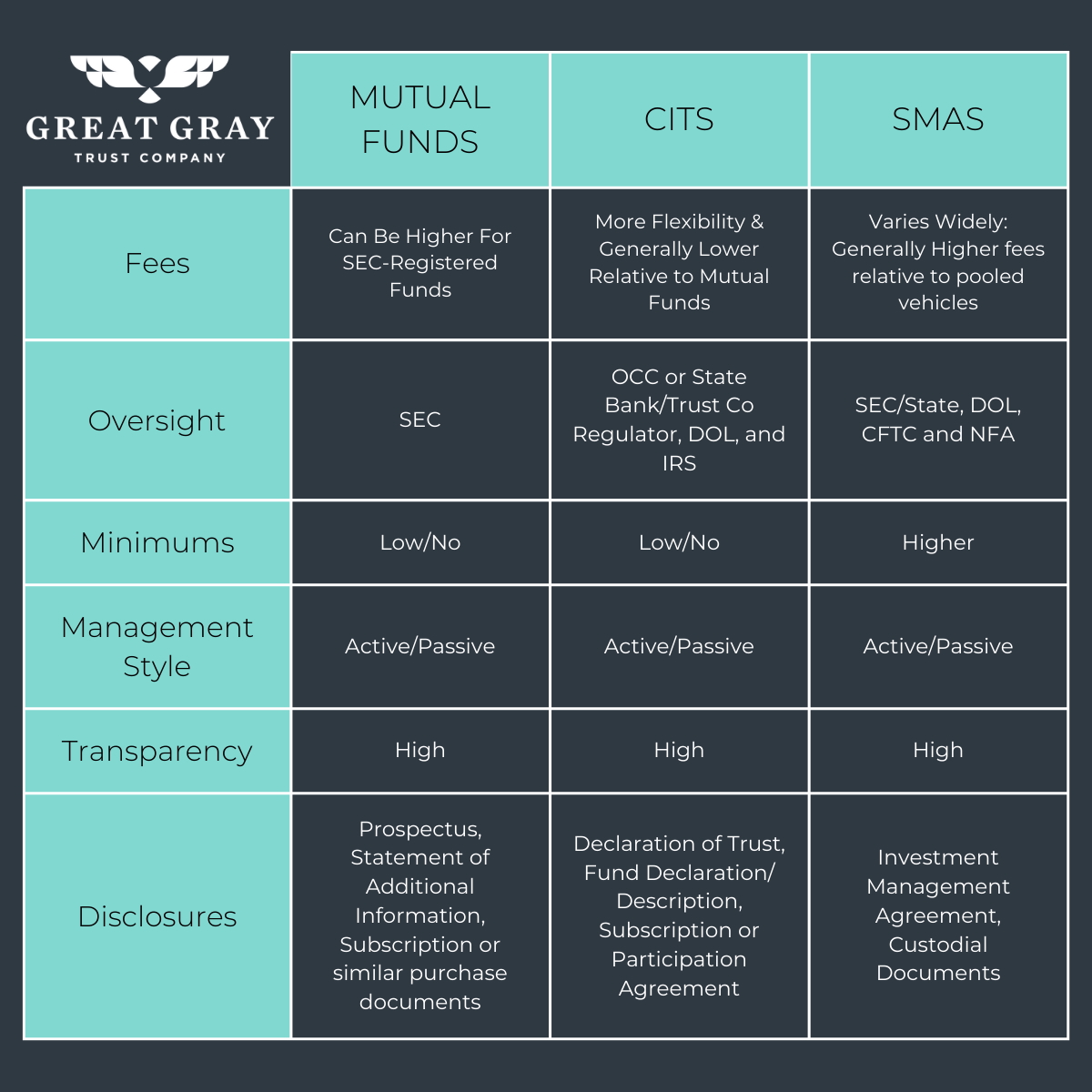

CITs often deliver meaningful cost savings without compromising on regulatory oversight or investor protections. According to the Morningstar 2025 Retirement Plan Landscape Report CITs average 23.9 basis points for active management compared to 60.1 basis points for mutual funds and provide approximately 50% savings on fees for passively managed funds.

These cost savings are driven by the different markets in which CITs and mutual funds serve – and explain why CIT’s cost savings come with investor protections, not at their expense. CITs are exclusively available to institutional, tax-qualified investors like 401(k) plans, and must comply with legal requirements and a regulatory regime that is specifically designed for retirement plan investors. By contrast, mutual funds can be sold to all types of investors, including individual retail investors. Mutual funds’ widespread distribution has prompted regulation that accounts for everyone but is not tailored for any particular investor segment. As a result, CITs not only provide cost advantages because of their specific focus on the retirement plan market, but they also offer protections tailored specifically for retirement plan participants.

CITs’ tailored protections arise from a regulatory regime that is focused on the retirement plan market. CITs are strictly regulated under state or federal banking laws, trust law, and, importantly, the U.S. Employee Retirement Income Security Act of 1974 (“ERISA”). Under ERISA, the CIT trustee and other investment managers are subject to the law’s full array of fiduciary duties, described by appellate courts as “the highest known to the law.” They are also required to comply with ERISA’s strict “prohibited transaction” rules designed to address potential conflicts of interest. By contrast, a mutual fund manager is not subject to ERISA’s fiduciary obligations or prohibited transaction rules, and the assets of the mutual fund are not considered ERISA plan assets, even if an ERISA plan invests in the mutual fund. This difference results in enhanced protections for plans and participants that invest in a CIT.

There has been a rapid reduction in barriers to access CITs. Over the last five years, investment minimums for CITs have been dramatically reduced or even eliminated. In addition, the vast majority of investment managers that offer strategies – spanning active and passive management – in mutual fund vehicles are now available in CIT vehicles. Great Gray currently offers more than 790 CITs across a broad array of asset classes and management styles. It is now possible for even the smallest retirement plans to craft a diversified menu of investment options, including passive and active management styles, consisting entirely of CITs.

Another driver of the uptick in CIT usage? CITs are transparent. In my experience, retirement plan decisionmakers and participants have no difficulty obtaining disclosures they need to make investment decisions about CITs.

Department of Labor (“DOL”) regulations require disclosure of the key information that participants need to make investment decisions in a standardized table: e.g., investment objective, asset class, performance over standardized periods against a relevant benchmark. These disclosure obligations apply equally for CITs, mutual funds, and any other investment vehicle. In addition, fact sheets are commonly made available on recordkeeper websites that are accessible when participants click a link to learn more about a fund. These fact sheets mirror the DOL-mandated disclosures, offering a clear, standardized snapshot of key details—performance, investment objective, risks, and underlying holdings. As above, the content is provided in a vehicle agnostic format – participants will receive the same key information, regardless of whether the investment is in a CIT, mutual fund, or other investment vehicle.

Great Gray Trust Company, LLC Collective Investment Funds (“Great Gray Funds”) are bank collective investment funds; they are not mutual funds. Great Gray Trust Company, LLC serves as the Trustee of the Great Gray Funds and maintains ultimate fiduciary authority over the management of, and investments made in, the Great Gray Funds. Great Gray Funds and their units are exempt from registration under the Investment Company Act of 1940 and the Securities Act of 1933, respectively.

Investments in the Great Gray Funds are not bank deposits or obligations of and are not insured or guaranteed by Great Gray Trust Company, LLC, any bank, the FDIC, the Federal Reserve, or any other governmental agency. The Great Gray Funds are commingled investment vehicles, and as such, the values of the underlying investments will rise and fall according to market activity; it is possible to lose money by investing in the Great Gray Funds.

Participation in Collective Investment Trust Funds is limited primarily to qualified retirement plans and certain state or local government plans and is not available to IRAs, health and welfare plans and, in certain cases, Keogh (H.R. 10) plans. Collective Investment Trust Funds may be suitable investments for plan fiduciaries seeking to construct a well-diversified retirement savings program. Investors should consider the investment objectives, risks, charges, and expenses of any pooled investment fund carefully before investing. The Additional Fund Information and Principal Risk Definitions (PRD) contains this and other information about a Collective Investment Trust Fund and is available at www.greatgray.com/cit-fund-info/principal-risk-definitions/ or ask for a free copy by contacting Great Gray Trust Company, LLC at (866) 427-6885.

Great Gray® and Great Gray Trust Company are service marks used in connection with various fiduciary and non-fiduciary services offered by Great Gray Trust Company, LLC.