- CIT Solutions

-

A Superior Collective Investment Trust Onboarding Experience.

-

- Perspectives

- About

- Reach out

A Superior Collective Investment Trust Onboarding Experience.

A Superior Collective Investment Trust Onboarding Experience.

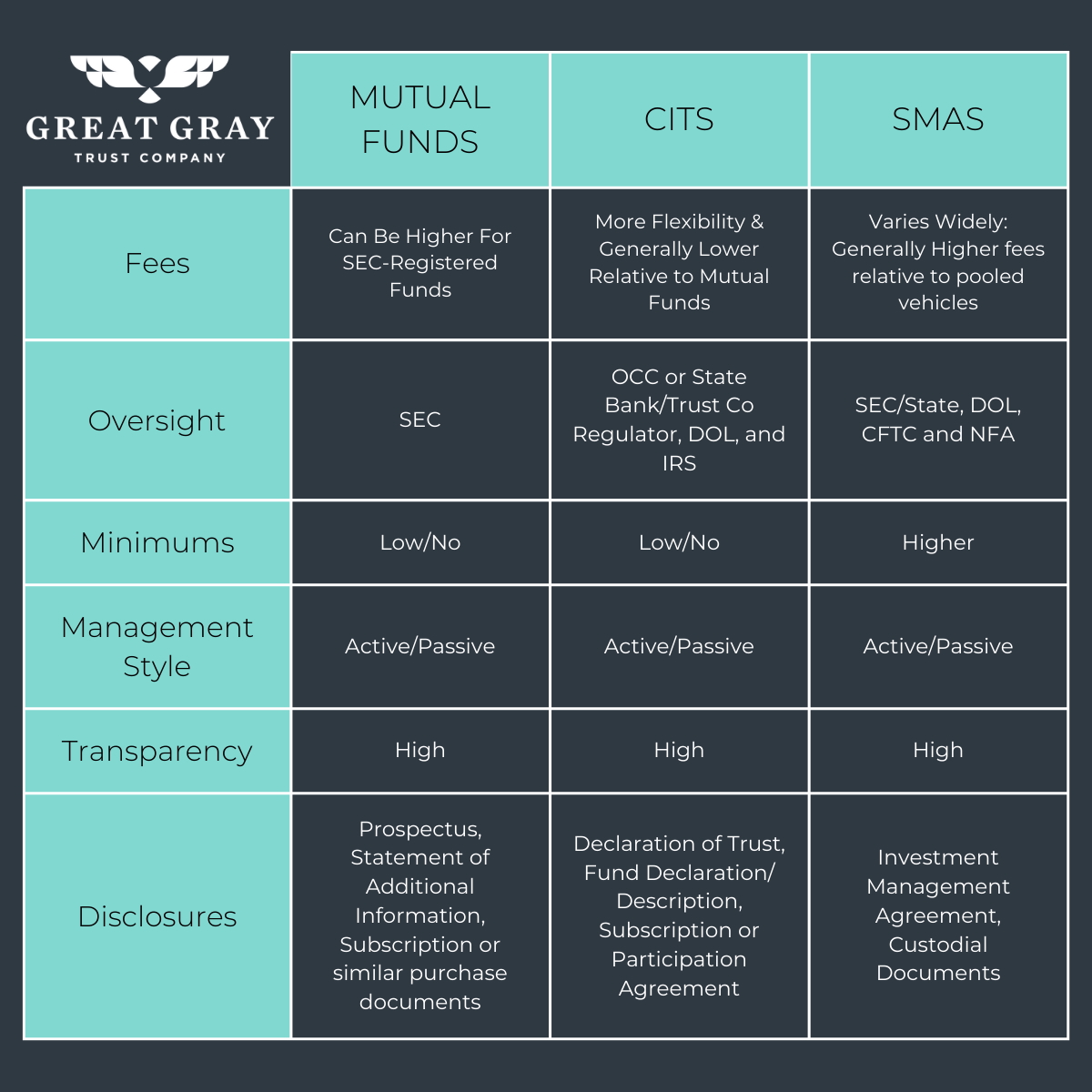

Collective Investment Trusts (CITs) and mutual funds are two popular pooled investment vehicles used as investment options for plan participants within their retirement plans. While both are strictly regulated, transparent, and can help plan participants reach their retirement goals, there are important differences between CITs and mutual funds, including who regulates them, their fee structures, tax structure, investor eligibility, and reporting standards. Chief among these differences, CITs often confer meaningful cost savings compared to mutual funds and are subject to legal oversight regime specifically designed for retirement plans.

CITs are strictly regulated investment vehicles in which tens of millions of Americans invest to save for their retirement. CITs are pooled investments much like mutual funds, except CITs are tax-exempt and are maintained by fiduciary trustees pursuant to laws and regulations focused on the retirement plan market.

Unlike mutual funds, CITs are only available to institutional, tax-qualified investors like 401(k) plans. CITs combine assets from retirement plan investors into a fund which is invested according to its stated objective. The trustee oversees the investments made in the CIT and holds primary fiduciary responsibilities. Subject to its ultimate oversight, a trustee may engage a third-party investment manager to invest the CIT assets according to a particular agreed-upon strategy. CITs are used as retirement plan options by plan advisors, responsible plan fiduciaries, and other decisionmakers overseeing tax-qualified, institutional retirement plans like 401(k)s.

While CITs and mutual funds both invest in passive and active portfolios of stocks and bonds, mutual funds generally have a higher cost structure and are overseen by a board that hires a registered investment adviser to manage the assets. Mutual funds must be sold through a registered broker-dealer, and are offered to retail as well as institutional investors through a variety of distribution and intermediary channels. Mutual funds cannot vary their management fee but can create separate share classes to vary their distribution and servicing fees. They may offer a share class that has servicing fees priced for and targeted to the retirement market, but the mutual fund itself usually is sold via other share classes to the broader investment community.

CITs often have meaningfully lower fees and expenses than other pooled investment products like mutual funds. According to the latest Morningstar report, the average actively managed mutual fund is more than 2.6 times more expensive than the average actively managed CIT, and the average passively managed fund is more than 2 times more expensive than the average passively managed CIT. Compounded over time, these cost savings can result in substantially improved retirement outcomes. [1] The Department of Labor has recognized that, over a 35-year career, a 1% difference in fees and expenses reduces an individual’s retirement savings by 28%.[2] This means that for someone who otherwise would have saved $1 million by retirement would lose out on $280,000 of retirement savings – solely because the individual paid more for otherwise identical plan investments.

These cost savings are primarily driven by the difference in markets that CITs and mutual funds serve. CITs are not available to the retail public and are available only to retirement plans, which is a key difference in their regulatory and operational setup.

By contrast, mutual funds are designed for a broad investor base, including retail and institutional investors. Therefore, the U.S. Securities and Exchange Commission (SEC) rules that govern them are focused on protecting the least sophisticated investors by requiring extensive disclosures for all potential investors, whether retail or institutional. And because mutual funds must be sold by SEC-registered broker-dealers, they are subject to the Financial Industry Regulatory Authority’s conduct and marketing rules, which creates a layer of cost and regulatory obligations focused on the retail investor. In sum, because mutual funds are available directly to retail investors, they are subject to stringent and costly SEC and FINRA registration and marketing rules, specifically geared to providing an extra level of protection to less sophisticated, individual retail investors who are making the investment decisions on their own.

By contrast, CIT sales are more restricted. CITs are available only to institutional, tax-qualified investors like retirement plans. CITs are subject to a stringent regulatory regime designed to protect retirement investors — but aren’t required to meet the more onerous obligations that apply to funds sold directly to retail investors because they can only be selected by an investment fiduciary or other responsible decisionmaker for a retirement plan. Accordingly, the disclosure requirements are tailored to the decisionmaker that selects the CIT as an investment option in the retirement plan. As a result, CITs experience lower regulatory expenses, leading to the reduced overall costs for retirement plan investors described in the most recent Morningstar report.

2. Regulatory Oversight

CITs and mutual funds differ in the ways that they are governed. CITs are subject to separate, overlapping regulatory regimes – State and/or Federal banking laws, the Internal Revenue Code (with regard to their tax-exempt status), the Department of Labor (DOL), and common law trust and fiduciary duty; they are also subject indirectly to Federal securities laws through the obligation to comply with exemptions from those laws.

Critically, CITs also are subject to Employee Retirement Income Security Act of 1974 (ERISA), resulting in enhanced investor protections. Because they can be offered only to retirement plans, virtually all CITs accept investments from plans that are subject to ERISA. If an ERISA plan invests in a CIT, the CIT, its trustee and its investment manager are subject to the law’s full array of fiduciary duties, described by appellate courts as “the highest known to the law.”[3] They are also required to comply with ERISA’s strict “prohibited transaction” rules and must make fulsome disclosures concerning the fees and other amounts charged to benefit plan investors or otherwise received by them. By contrast, the assets of a mutual fund are not considered ERISA plan assets, and therefore the manager of a mutual fund in which a plan invests is not subject to ERISA’s fiduciary obligations.

Unlike CITs, mutual funds are regulated directly by the SEC under Federal securities laws and generally not by the overlapping bodies of law and regulators that govern CITs. Mutual fund investment managers hold responsibility for making investment decisions in line with the goals outlined in the fund’s prospectus. Unlike CITs, which are governed by trustees that must adhere to the regulatory regime founded on fiduciary principles arising under ERISA, state or federal banking law, and common law, mutual funds are governed by boards of directors that are required to include independent directors.

3. Eligibility for Investors

Mutual funds are available for purchase by the general public and generally sold by brokers to retail investors. To address potentially volatile cash flows, mutual funds may be subject to redemption fees whereas CITs generally do not impose such fees because retirement plan investors are generally long-term investors, and the CIT trustee has sophisticated tools and options for managing liquidity and mitigating any adverse cash flow impacts on investors in the CIT.

By contrast, CITs are restricted under tax laws to qualified retirement plans, including tax-qualified corporate plans like 401(k)s and some state and local government plans. This allows CITs to enjoy tax-exempt status. To maintain their tax-free status, it is essential for trustees to verify plan eligibility, which they do by having the retirement plan enter into a “participation agreement” or an “adopting agreement” so the trustee can collect information to confirm a plan’s eligibility. The participation or adoption agreement typically also documents the trustee’s fiduciary obligations under ERISA.

4. Transparency and Reporting Standards

In the past, some have criticized CITs as being non-transparent, but this is not the case. Both CITs and mutual funds are transparent and provide retirement plan decisionmakers and participants with fulsome information needed to make investment decisions. Since 2011, DOL regulations have mandated standardized disclosures of the key information to facilitate investment decisions for all investments in a participant-directed defined-contribution plan, regardless of the type of investment vehicle (i.e., mutual fund, CIT, annuity, etc.). These requirements obligate clear disclosure of the investment’s cost, the type of investment and objective, and the investment performance over standardized periods compared with an appropriate benchmark.

A retirement plan participant generally has access to fact sheets describing a CIT’s key investment information on the plan recordkeeper’s website in the same way the participant would access key investment information about a mutual fund. Likewise, participants see the daily value of the CIT updated in the same manner as mutual fund valuations. Finally, these disclosures have been supplemented with other types of general market reporting as a result of advancements in streaming data and real-time reporting. A notable milestone occurred in 2019, when Great Gray’s President and CEO Rob Barnett (in his prior role with Great Gray’s predecessor) introduced the first CIT tickers listed on the NASDAQ, marking a new era of transparency and accessibility for investors and plan advisors. This innovation allows investors to track daily CIT prices and performance through aggregators such as Morningstar, Fi36o, BrightScope, and many other reporting systems. In addition, Morningstar began tracking and reporting on CITs from 2007, and it now covers approximately 7,800 CITs. Using this information, retirement plan fiduciaries and their advisers can analyze CITs in comparison to competing investment options, including similarly managed mutual funds.

While mutual funds also have transparency features like tickers, they serve a much broader public market and generally are not structured specifically for retirement investors. CITs offer the advantage of purpose-built retirement solutions at generally lower costs, alongside operational standards such as daily NAV pricing, quarterly performance reporting, fund fact sheets, and other modern transparency features to align with those offered through mutual funds.

While CITs share many key attributes with mutual funds, they offer unique advantages. Given the lower-cost structure and price flexibility of CITs, they are an attractive option for tax-qualified retirement plans such as 401(k)s. These cost savings come without loss of investor protections because CITs are subject to a regulatory regime that is specifically designed for retirement plan investors. These advantages help explain why CITs recently surpassed mutual funds as the most popular investment vehicle in defined contribution retirement plans – with CITs used by 82% of defined contribution plans. [4]

Great Gray Trust Company, LLC Collective Investment Funds (“Great Gray Funds”) are bank collective investment funds; they are not mutual funds. Great Gray Trust Company, LLC serves as the Trustee of the Great Gray Funds and maintains ultimate fiduciary authority over the management of, and investments made in, the Great Gray Funds. Great Gray Funds and their units are exempt from registration under the Investment Company Act of 1940 and the Securities Act of 1933, respectively.

Investments in the Great Gray Funds are not bank deposits or obligations of and are not insured or guaranteed by Great Gray Trust Company, LLC, any bank, the FDIC, the Federal Reserve, or any other governmental agency. The Great Gray Funds are commingled investment vehicles, and as such, the values of the underlying investments will rise and fall according to market activity; it is possible to lose money by investing in the Great Gray Funds.

Participation in Collective Investment Trust Funds is limited primarily to qualified retirement plans and certain state or local government plans and is not available to IRAs, health and welfare plans and, in certain cases, Keogh (H.R. 10) plans. Collective Investment Trust Funds may be suitable investments for plan fiduciaries seeking to construct a well-diversified retirement savings program. Investors should consider the investment objectives, risks, charges, and expenses of any pooled investment fund carefully before investing. The Additional Fund Information and Principal Risk Definitions (PRD) contains this and other information about a Collective Investment Trust Fund and is available at www.greatgray.com/cit-fund-info/principal-risk-definitions/ or ask for a free copy by contacting Great Gray Trust Company, LLC at (866) 427-6885.

Great Gray® and Great Gray Trust Company are service marks used in connection with various fiduciary and non-fiduciary services offered by Great Gray Trust Company, LLC.

{kind=link}