- CIT Solutions

-

A Superior Collective Investment Trust Onboarding Experience.

-

- Perspectives

- About

- Reach out

A Superior Collective Investment Trust Onboarding Experience.

A Superior Collective Investment Trust Onboarding Experience.

A top question knowledgeable employer plan fiduciaries ask retirement plan advisors is what cash preservation vehicle should be used in the plan lineup. In general, there are two options: stable value funds and money market funds.¹ Here are three key insights every retirement plan advisor should keep in mind when considering stable value fund solutions:

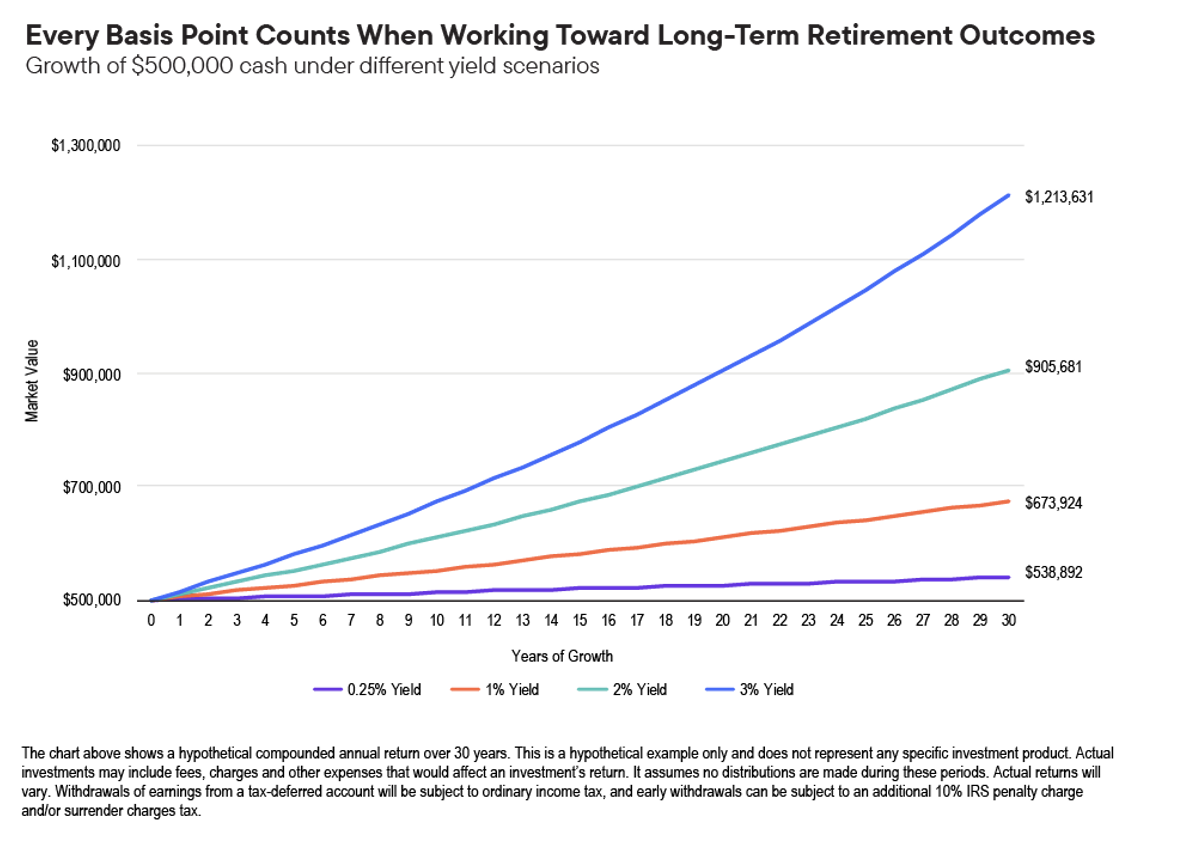

Given its relatively lower risk profile, likely returns for a cash preservation vehicle are smaller than those of an equity or fixed income investment– but that does not make the decision to select the cash preservation investment option in a plan lineup any less consequential. Legally, the same investment standard applies consistently across asset classes for retirement plans covered by the Employee Retirement Income Security Act of 1974 (ERISA). A cash preservation investment option, like an investment in any other asset class, should be selected for inclusion in a plan lineup for the sole purpose of maximizing risk-adjusted financial returns.

For participants who remain consistently invested in a cash preservation vehicle, the decision as to which investment option can be consequential. Just as the cost savings afforded by collective investment trusts can have profound impacts on retirement security, even seemingly small increases in yields can compound over a course of a career to result in tens or even hundreds of thousands of dollars in additional amounts available in retirement.

Why stable value is critical in retirement plan menus, Franklin Templeton

So don’t let down your guard because cash preservation is “unsexy” or because its potential investment returns are smaller than riskier asset classes. Deciding between a stable value or money market fund and selecting the plan’s cash preservation investment option should be supported by a robust fiduciary process to identify the option that will maximize risk-adjusted financial returns for plan participants and beneficiaries.

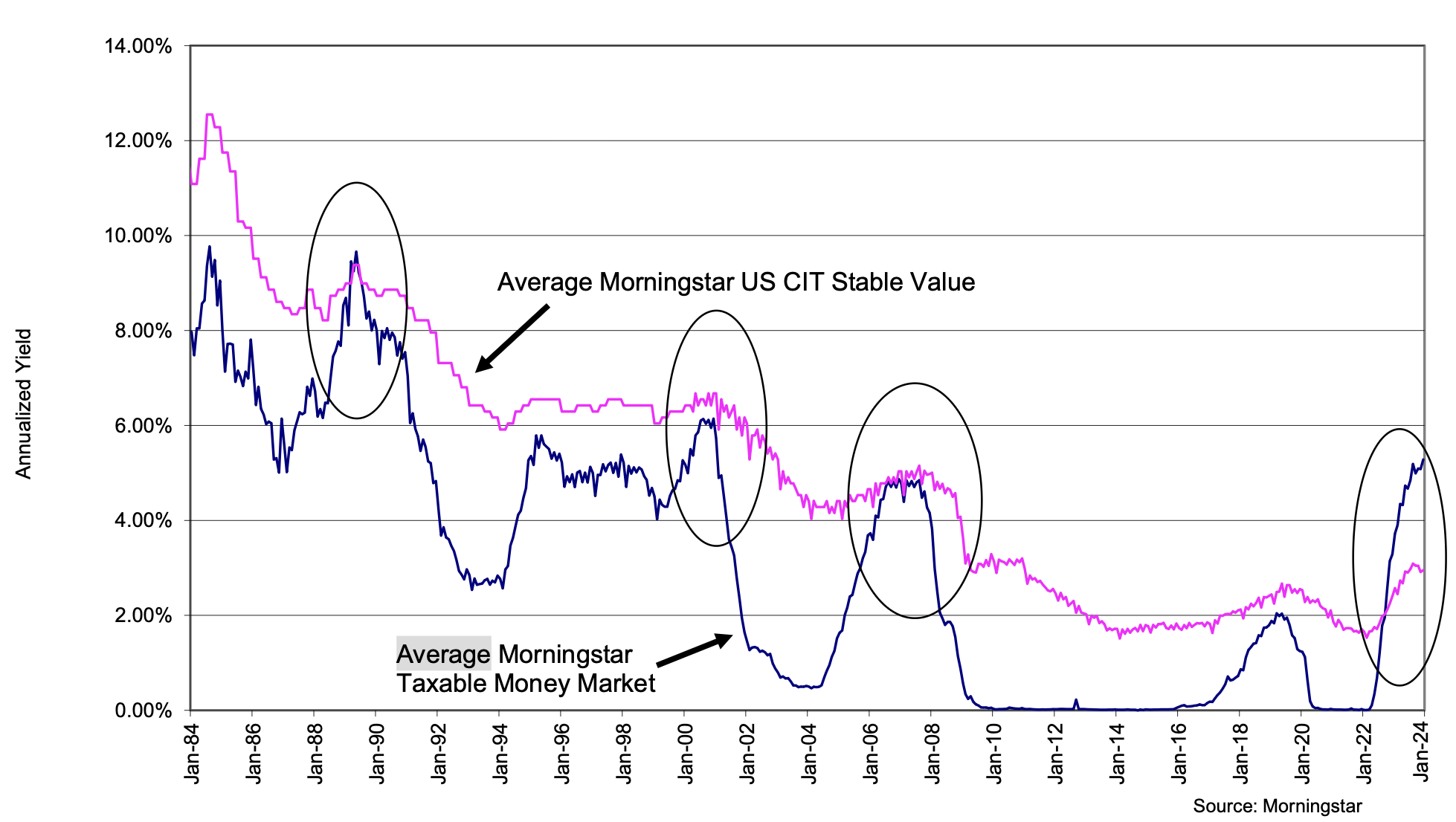

Stable value is the dominant cash preservation vehicle in employer-sponsored defined contribution plans, with approximately 82% of plans offering it according to a recent study.² This level of usage is consistent with stable value’s historical outperformance of money market funds over extended periods of time.

More Worth Knowing About Stable Value Funds, The Standard, 2025

As reflected in this chart, there have been only a few periods when stable value has not outperformed money market funds, although one such period has been in recent years. A key factor in understanding stable value’s general outperformance is the duration of fixed income products underlying each investment vehicle.

In general, stable value funds invest in longer-maturity, fixed income products, like intermediate-term bonds. By contrast, money market funds generally invest in short-term investments, like three-month U.S. Treasury bills. Over longer periods of time, the general trend is for longer maturity fixed income products to produce higher yields – an outcome reflected in in the considerable outperformance by stable value funds from approximately 2008 to 2022.

An exception arose during the Fed’s aggressive monetary tightening efforts beginning in 2022. These efforts resulted in outperformance by money market funds, as the yield curve inverted with shorter duration investments yielding higher returns than longer ones. This recent outcome is not surprising given money market funds’ shorter duration investments. However, it may be reasonable to expect stable value funds to outperform money market funds in future years in a more typical interest rate environment when long-term yields are higher than short-term yields.

ERISA does not require the selection of a single “best” stable value investment option that, with the benefit of hindsight, outperformed alternatives. Rather, a prudent process should be undertaken to select an investment option that is reasonably determined to maximize risk-adjusted financial returns.

To support this process, advisors should undertake detailed analysis of the risk and return characteristics of stable value funds. For example, advisors may want to analyze factors including:

The selection of a cash preservation investment option is consequential – and requires detailed analysis. If you’re ready to discuss how stable value solutions can fit in your retirement plan lineups, contact your region’s Qualified Plan Specialist today.

¹ Money market funds can be in the form of a money market mutual fund or a money market CIT (also called a STIF or short-term investment fund under OCC Regulation 9.18(b)(4)(iii)). What differentiates stable value funds from money market funds is that stable value funds usually have an insurance component. For more information about stable value funds, see Stable Value at a Glance – Stable Value Investment Association.

² MetLife Stable Value Study, 2024

Great Gray Trust Company, LLC Collective Investment Funds (“Great Gray Funds”) are bank collective investment funds; they are not mutual funds. Great Gray Trust Company, LLC serves as the Trustee of the Great Gray Funds and maintains ultimate fiduciary authority over the management of, and investments made in, the Great Gray Funds. Great Gray Funds and their units are exempt from registration under the Investment Company Act of 1940 and the Securities Act of 1933, respectively.

Investments in the Great Gray Funds are not bank deposits or obligations of and are not insured or guaranteed by Great Gray Trust Company, LLC, any bank, the FDIC, the Federal Reserve, or any other governmental agency. The Great Gray Funds are commingled investment vehicles, and as such, the values of the underlying investments will rise and fall according to market activity; it is possible to lose money by investing in the Great Gray Funds.

Participation in Collective Investment Trust Funds is limited primarily to qualified retirement plans and certain state or local government plans and is not available to IRAs, health and welfare plans and, in certain cases, Keogh (H.R. 10) plans. Collective Investment Trust Funds may be suitable investments for plan fiduciaries seeking to construct a well-diversified retirement savings program. Investors should consider the investment objectives, risks, charges, and expenses of any pooled investment fund carefully before investing. The Additional Fund Information and Principal Risk Definitions (PRD) contains this and other information about a Collective Investment Trust Fund and is available at www.greatgray.com/cit-fund-info/principal-risk-definitions/ or ask for a free copy by contacting Great Gray Trust Company, LLC at (866) 427-6885.

Great Gray® and Great Gray Trust Company are service marks used in connection with various fiduciary and non-fiduciary services offered by Great Gray Trust Company, LLC.